How to Get Cheap Car Insurance Safely

If you’re paying too much for your policy, finding cheap car insurance might feel like chasing the white whale. But don’t despair — there are proven, research-backed ways to lower premiums and keep strong protection. Common levers include right‑sizing your deductibles (moving from a $500 to $1,000 auto deductible often lowers overall premiums about 5–10%, and going to $2,000 can be roughly 12–20% on average) according to national analyses from The Zebra (2025) and Bankrate (2025), enrolling in telematics/usage‑based insurance where you’re a consistently safe or lower‑mileage driver (LexisNexis 2024 Trends), and taking advantage of advance‑quote/early‑signing style discounts offered by many carriers (availability and amounts vary by state/program; see examples from Allstate, Nationwide, Travelers, Liberty Mutual, and American Family in the Pro Tip below). In fact, we’ve already detailed the eight best ways to save on car insurance.

That said, there are also plenty of things you shouldn’t do when trying to save on car insurance. Cutting coverage too far, misstating facts on your application, or choosing a deductible you can’t afford can backfire. And contrary to some viral tips, there isn’t a reliable “cheapest month” to buy auto insurance; current evidence shows pricing is driven by loss costs and regulatory filings over time rather than month‑of‑year effects (BLS CPI methodology; CCC Crash Course 2025). Take a moment to learn about the five most common cheap car insurance mistakes and make sure you’re protected where it counts.

1. Don’t cut coverage in order to cut costs

Oftentimes, people equate “cheap car insurance” with “buying the minimum legal limits.” That can be risky because state minimums vary, have changed in several places, and often don’t cover serious losses. For example, California’s minimum liability increased to 30/60/15 for policies effective January 1, 2025, with another step to 50/100/25 scheduled for 2035 (California Vehicle Code §16056). Virginia’s minimums increase to 50/100/25 in 2025 and the state eliminated its uninsured motor vehicle fee on July 1, 2024 (Virginia DMV). New Jersey raised Standard Policy minimums in 2023 and increases bodily injury minimums again in 2026 to 35/70 (property damage remains 25) (NJ DOBI). Requirements also differ by regime: Florida requires PIP $10,000 and PDL $10,000 but generally not BI liability (FLHSMV); New York requires liability 25/50/10, PIP $50,000, and UM at least 25/50 (NY DMV); Texas requires 30/60/25 (Texas DOI); New Hampshire doesn’t mandate auto insurance but expects drivers to meet financial responsibility if they cause a crash (NH DMV).

Justin Lovely, a personal injury lawyer at The Lovely Law Firm, shares this rule of thumb for choosing the right coverage levels: “An easy way to figure it out is to determine how much property you have. For instance, if you own a $300k home, a $50k boat, and two cars at $50k, you need to have liability insurance for $400k, the value of your potential assets to lose.” In practice, many drivers choose limits higher than the legal minimum so one at‑fault crash doesn’t expose savings or future wages. If you live in a no‑fault/PIP state or one that mandates UM, verify the required first‑party benefits and UM/UIM on your state’s official page (e.g., Florida; New York).

Pro tip: When requesting quotes online, most companies let you toggle limits to see the price impact. Use your state’s published minimums as a baseline, then quote higher limits and add‑ons like UM/UIM or PIP where applicable. Official pages (e.g., Virginia DMV, California law, NJ DOBI) clarify what’s required now and what’s scheduled to change.

2. Never bend the truth on your application

It might be tempting to fudge the numbers just a little on your car insurance application. You could save by leaving off that pesky speeding ticket, for example, or answering “yes” to a few discounts you don’t actually qualify for.

Here’s the thing: It doesn’t work. Insurers verify applications using driver record data and specialty consumer reports such as CLUE for prior auto/property claims (CFPB: specialty consumer reports). Material misrepresentation can trigger re‑rating, cancellation/nonrenewal, claim denials, or policy rescission under state property/casualty law. Representative statutes: New York permits avoidance for a material misrepresentation that would have affected issuance or price (NY Ins. Law §3105), and California allows rescission for material concealment or false material representation even if unintentional (Cal. Ins. Code §331). Application fraud is a crime in every state (NAIC). Life and health insurers also use MIB to flag inconsistencies (consumers can request their file) (MIB), and while that database focuses on life/health, the takeaway is the same: data‑driven checks make it likely that misstatements will be found.

3. Avoid a deductible that you couldn’t pay today

Choosing a higher collision or comprehensive deductible is one of the most common ways to save on car insurance. Deductibles can be as high as $2,000, though customers generally see the biggest savings when jumping from $500 to $1,000. Current market data shows roughly 5–10% lower overall premiums on average when moving from a $500 to $1,000 auto deductible, and about 12–20% when moving from $500 to $2,000—your results vary by state, company, and how much of your premium is in physical damage coverages (The Zebra 2025; Bankrate 2025). Deductible changes affect collision/comprehensive only; liability, PIP/MedPay, and UM/UIM premiums are unaffected (Triple‑I).

For those that are on the fence, think about it this way: a lower deductible typically means a higher premium spread across the year, while a higher deductible requires you to produce more cash at claim time. If paying a $1,000 or $2,000 deductible today would create hardship, the “savings” from choosing it can vanish quickly if you need repairs after a loss.

If a bigger deductible would take a toll on your wallet (and potentially leave you without transportation), then it makes sense to pay a little more each year and protect yourself in the event that you have to file a claim. Savings also vary by market and insurer, and very high deductibles may not be available in every state or program, so ask your agent to quote several options side‑by‑side to see your personal curve (Bankrate 2025; The Zebra 2025).

4. Forget the idea of a ‘cheaper’ time to insure

You may have heard that it’s cheapest to buy car insurance during a certain month or season. One older study by InsuranceQuotes.com has been widely cited, but up‑to‑date evidence shows personal auto pricing in 2025 is dominated by loss‑cost inflation and regulatory rate filings rather than consistent month‑of‑year discounts. The Bureau of Labor Statistics explains that motor vehicle insurance changes are reflected as policies renew over time, dampening any simple “buy in month X” savings pattern (BLS CPI methodology). Repair and total loss costs have remained elevated post‑pandemic, pushing rates across months rather than creating predictable seasonal discounts (CCC Crash Course 2025).

While individual experiences vary by driver, vehicle, and location, industry tracking shows seasonality more in shopping volumes and marketing than in base prices. In short, there’s no robust, repeatable “cheapest month” for consumers in current data; prices move with filings and underwriting cycles, not the calendar.

In reality, the best time to buy car insurance is when you purchase a new vehicle or when your current policy expires. It’s important to be insured right away. Not only is it impossible to know when an accident might occur, but trying to time the market can leave you uninsured or underinsured. Maintaining continuous coverage also helps many shoppers avoid lapse‑related surcharges.

Pro tip: Instead of searching for the “cheapest” month, shop before your policy expires and look for advance‑quote/early‑signing style discounts tied to getting a quote and/or binding days before the effective date. Examples: Allstate (Early Signing), Nationwide (Advance Quote – e.g., at least 8 days before the effective date), Travelers (Early Quote), Liberty Mutual (Early Shopper), and American Family (Early Bird). These incentives are filed by state, amounts vary by program, and not all carriers offer them (e.g., GEICO does not list an advance‑quote discount). If you drive safely and fewer miles, also consider telematics/usage‑based programs that provide an enrollment discount and then adjust at renewal based on behavior (LexisNexis 2024 Trends).

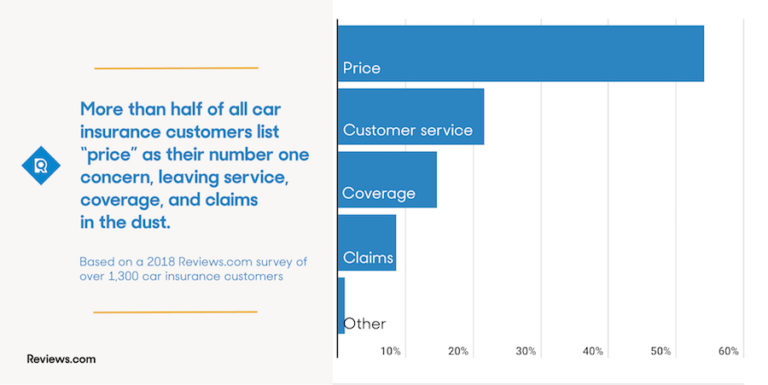

5. Don’t let price be your only consideration

Price is likely to be the deciding factor between any two companies with similar coverage. However, it shouldn’t be the only thing you consider when comparing insurers. There’s a lot to be said for companies with a strong customer service record and good claims handling, too. Recent studies show auto claims satisfaction improved modestly year over year but still trails pre‑pandemic highs; communication quality, settlement clarity, and repair timeliness drive the biggest differences in experience (J.D. Power 2024).

“You can buy cheap insurance anywhere” says John Espenschied, Agency principal and owner of Insurance Brokers Group. “But if you find out that the provider isn’t able to adequately handle your claim, you might be disappointed in the settlement if and when you need to use your insurance.”

Before committing to an insurer based on price alone, check out its track record. You can vet customer satisfaction through Consumer Reports’ auto insurance survey and find claims handling scores at J.D. Power. Corroborate performance with the NAIC complaint index. If a company’s ratings make you squirm, it’s worth looking into other options. Service may mean the difference between a smooth, easy claims payout and a paperwork nightmare that only adds to the stress of an accident.

Pro tip: Skip the legwork and check out our review of the best cheap auto insurance, where we’ve evaluated top providers based on service, claims satisfaction, coverage, discounts, and more.

The Bottom Line

When it comes to car insurance, some things are simply given: Younger drivers pay more than older drivers, risky drivers pay more than safe ones, and bare-bones policies cost less but also pay less after a disaster. There’s no reliable “cheapest month” to buy coverage in current data; pricing reflects loss costs and regulatory filings that flow through renewals over time (BLS CPI; CCC Crash Course 2025). Also remember that legal minimums vary by state and have changed recently in several places: California (30/60/15 effective 2025; 50/100/25 scheduled for 2035), Virginia (50/100/25 in 2025; UM fee eliminated 2024), and New Jersey (Standard Policy step‑up again in 2026) — verify details on your state’s site (CA; VA; NJ).

Luckily, there are plenty of ways that you can save on your car insurance. Shop around at renewal, avoid coverage gaps, consider telematics/usage‑based programs if you’re a safe or lower‑mileage driver (LexisNexis 2024 Trends), and evaluate higher deductibles only if you can afford them at claim time — moving from a $500 to $1,000 deductible typically reduces overall premiums about 5–10% on average, with larger jumps to $2,000 commonly around 12–20% (The Zebra 2025; Bankrate 2025). If you’re switching, plan ahead to qualify for advance‑quote/early‑signing style discounts where available (requirements and amounts vary by state/program; see carriers cited above).