If you sideswipe a parked car, cause a fender bender, or find yourself at-fault in a more serious collision, your insurance company will cover the other person’s injuries and damages. That’s what liability insurance is for. Conversely, if someone else hits you, their liability coverage should pay your losses — but many drivers carry low limits or no insurance at all, which is why UM/UIM protection matters.

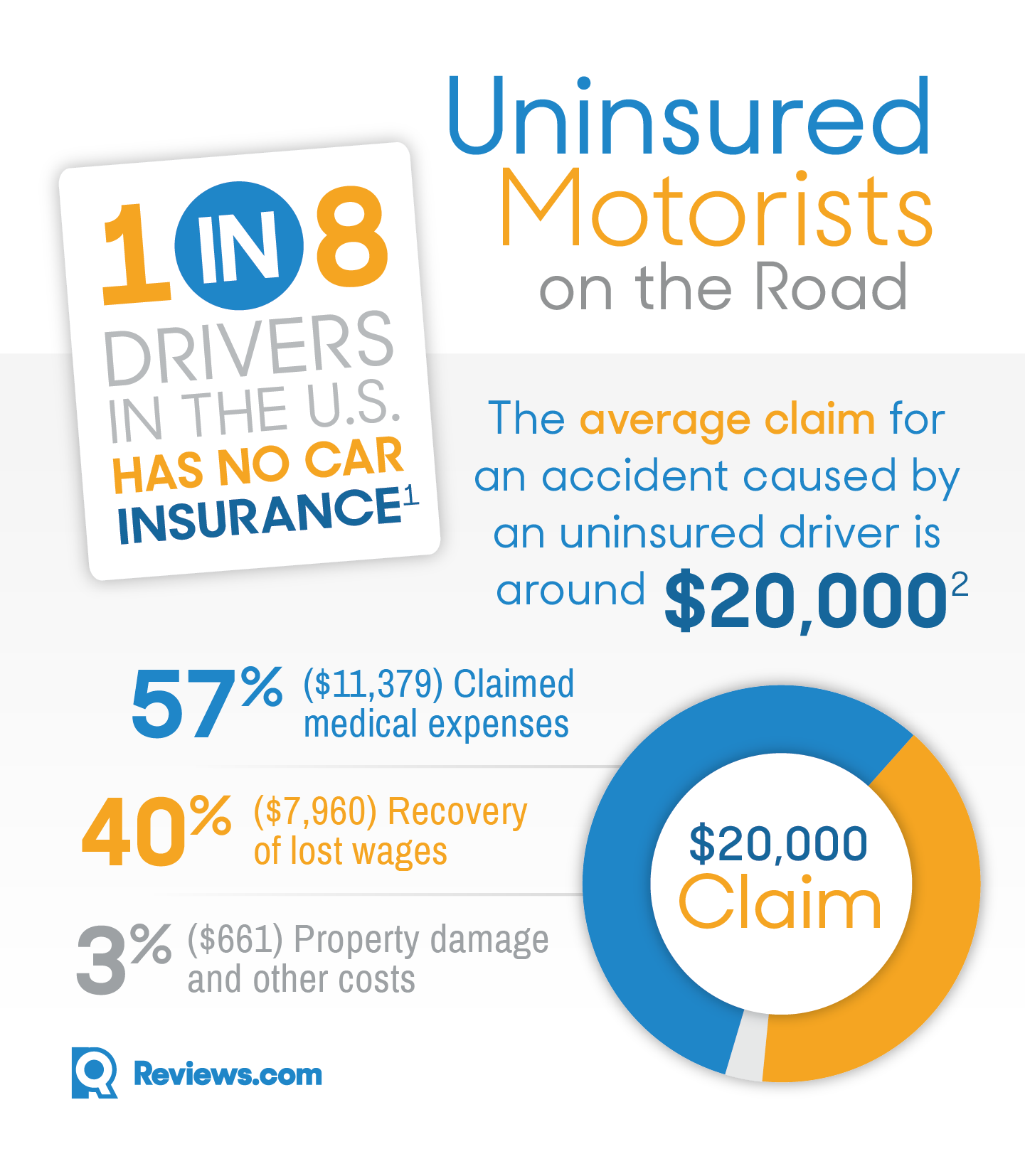

If you’re hit by a driver with no insurance or not enough to cover your costs — or it’s a hit-and-run where the at-fault driver can’t be identified — uninsured/underinsured motorist coverage can pay your medical and related damages up to your limits. Nationally, about 14% of motorists were uninsured in 2022 (roughly 1 in 7), with some states near or above 20%, according to the Insurance Information Institute summarizing Insurance Research Council estimates. At the same time, injury claim severities have risen since 2019, driven by medical and repair cost inflation, as documented in CCC Crash Course 2024 and LexisNexis’ 2024 U.S. Auto Insurance Trends Report.

What is Uninsured Motorist Coverage?

Uninsured motorist coverage (UM) pays when an at-fault driver has no liability insurance. In many states it also applies to certain hit-and-run crashes, typically subject to state-specific proof rules (for example, some jurisdictions require physical contact or corroborating evidence). See current state summaries from the Insurance Institute for Highway Safety and AAA’s Digest of Motor Laws for details. UM is generally split into bodily injury (UMBI) and, in some states, property damage (UMPD). With UMBI, your insurer can cover medical bills, lost wages, and related damages for you and your passengers; with UMPD (where offered), your insurer may help repair your vehicle, typically subject to a deductible. Without UM, these costs can fall to you if the other driver lacks insurance.

Context: Nationally about 14% of motorists were uninsured in 2022 (IRC estimate via the Insurance Information Institute). Injury and repair severities have increased since 2019, per CCC Crash Course 2024 and LexisNexis 2024.

Hit-and-run handling under UM and proof requirements vary; check state rules in IIHS and AAA’s Digest.

What Does Uninsured Motorist Insurance Cover?

Like liability insurance, UM coverage has two parts that may be purchased together or separately, depending on your state:

Uninsured motorist bodily injury (UMBI) pays for medical expenses, lost wages, and related damages for you and passengers when hit by an uninsured at-fault driver. In many states, UMBI also protects you as a pedestrian or cyclist and in qualifying hit-and-run crashes; specifics vary by law and policy terms. See the Insurance Information Institute’s UM/UIM explainer and Texas Department of Insurance consumer guidance.

Uninsured motorist property damage (UMPD) helps repair your vehicle when an uninsured driver damages it, where this coverage is available. A deductible (often around $250, but set by state/policy) may apply, and some states limit UMPD or require collision coverage instead. See Progressive’s UM/UMPD overview and your state consumer resources.

Many states that mandate UM require only UMBI and leave UMPD optional. If you drive a newer luxury vehicle, an EV, or a large SUV/truck — which tend to have higher repair costs due to ADAS calibration and complex parts — consider UMPD (or rely on collision) to protect your car. Industry reports show repair costs and calibration complexity rising, with EV repairable claim severity outpacing ICE vehicles (CCC Crash Course 2025; Mitchell EV Collision Insights Q2 2025).

Uninsured vs. Underinsured Motorist Coverage

Uninsured motorist (UM) pays when the at-fault driver has no liability insurance. Underinsured motorist (UIM) pays when the at-fault driver’s liability limits are insufficient to cover your damages; your UIM limits can close the gap up to the amount you select. This is especially important in states with lower minimum liability limits and in today’s higher-severity claim environment (CCC 2024; LexisNexis 2024).

UM/UIM rules vary by state. Examples: Minnesota and Oregon require both UM and UIM at minimum 25/50 BI limits (Minn. Stat. §65B.49; ORS 742.502). Massachusetts requires UM BI (20/40) and mandates UIM be offered (Mass. Gen. Laws c.175 §113L). Illinois requires UM BI 25/50 and UIM when your BI limits exceed the state minimum (215 ILCS 5/143a‑2). New York compels UM and requires supplementary UM/UIM (SUM) to be offered up to BI limits (N.Y. Insurance Law §3420(f)(2)). Virginia includes UM/UIM by default with limits equal to BI unless you reject or reduce them, and, effective 2023, UIM is add‑on (not reduced by the at‑fault driver’s limits) unless you opt out (Va. Code §38.2‑2206). For stacking and setoff rules, consult IIHS or AAA as provisions vary widely.

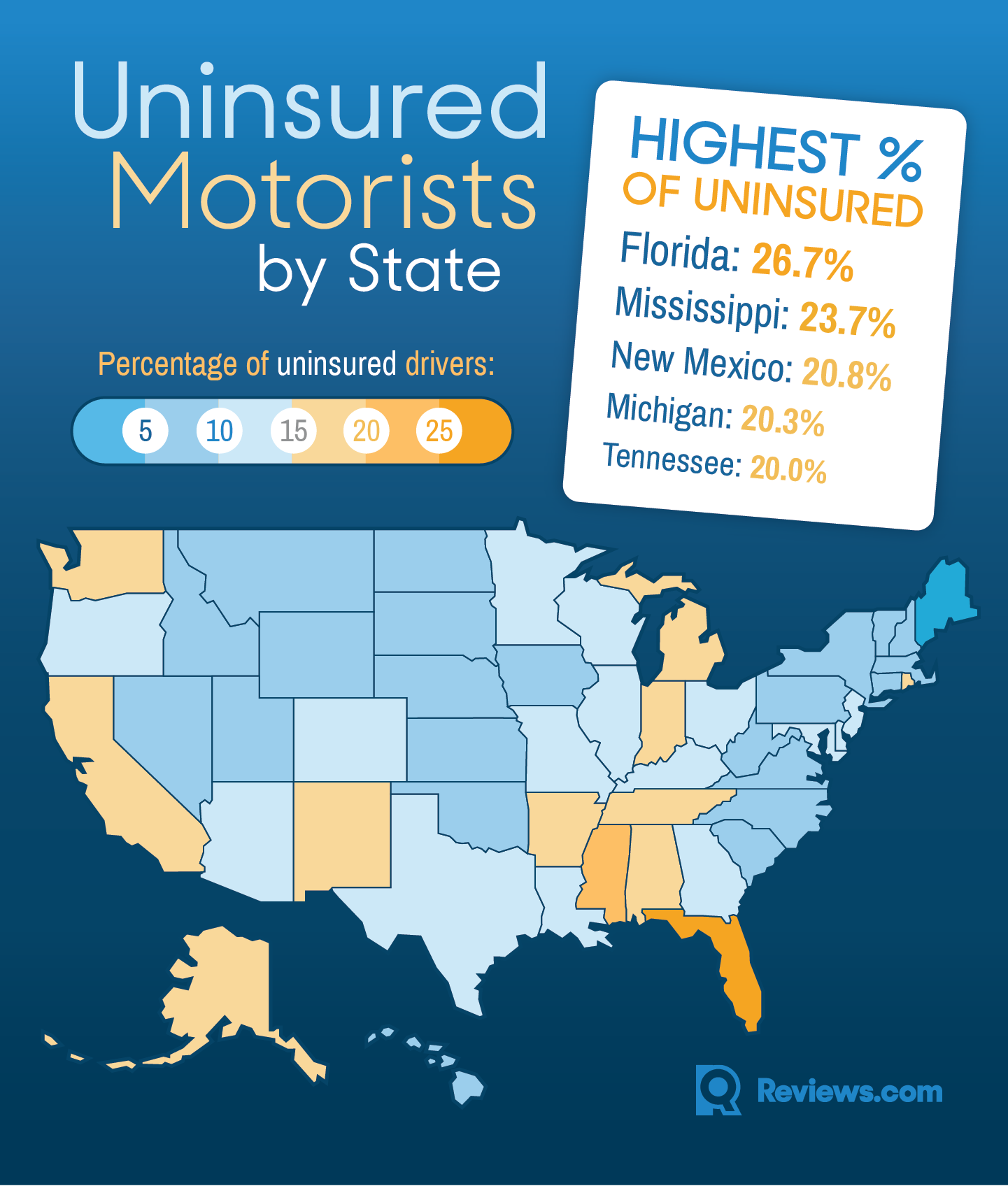

Latest available estimates show about 14% of U.S. motorists were uninsured in 2022, with large state variation (e.g., some states near 30% and others in low single digits), per the IRC as summarized by the Insurance Information Institute. For current state-by-state requirements and minimums, see IIHS and AAA.

How Much Does Uninsured/Underinsured Motorist Coverage Cost?

Updated 2024–2025 analyses place typical add-on costs for UM/UIM bodily injury around $100–$200 per year (about $8–$17 per month) for common limits, with UMPD — where available — often adding $40–$90 per year. Multiple sources align in the low-hundreds range, including NerdWallet (2025), ValuePenguin (2024–2025), Bankrate (2024–2025), and Forbes Advisor (2024–2025). On a full‑coverage policy, UM/UIM often represents roughly 4%–8% of premium. Prices vary widely by state and limits; in high‑uninsured or high‑severity markets, costs can exceed $300 per year. Broad auto insurance inflation through 2024–2025, reflected in BLS CPI, means older 2019 estimates (e.g., earlier CarInsurance.com figures) generally understate current pricing.

Is Uninsured Motorist Coverage Required?

Many states require UM, and a subset also require UIM; others mandate that insurers include or offer UM/UIM unless you reject in writing. Minimum limits typically mirror a state’s BI liability minimums (often 25/50; some states are higher). Examples today: Minnesota and Oregon mandate both UM and UIM at least 25/50 BI (Minn. Stat. §65B.49; ORS 742.502); Massachusetts requires UM BI (20/40) and requires insurers to offer UIM (§113L); Illinois requires UM BI 25/50 and UIM when BI limits exceed the minimum (215 ILCS 5/143a‑2); New York requires UM and SUM offers up to BI (§3420(f)(2)). Virginia includes UM/UIM by default and, since 2023, treats UIM as add‑on unless you opt for the reduced-by form (Va. Code §38.2‑2206). For a 50‑state snapshot and recent updates (including states adjusting minimum limits), consult IIHS and AAA. Note: Virginia also ended the option to drive uninsured by paying a fee for new registrations effective July 1, 2024, per NCSL.

| Minimum UMBI Coverage | Minimum UMPD Coverage | |

| Connecticut | 25/50 | |

| Washington, D.C. | 25/50 | 5 |

| Illinois | 25/50 | |

| Kansas | 25/50 | |

| Maine | 50/100 | |

| Maryland | 30/60 | 15 |

| Massachusetts | 20/40 | |

| Minnesota | 25/50 | |

| Missouri | 25/50 | |

| Nebraska | 25/50 | |

| New York | 25/50 | |

| North Carolina | 30/60 | 25 |

| North Dakota | 25/50 | |

| Oregon | 25/50 | |

| South Carolina | 25/50 | 25 |

| South Dakota | 25/50 | |

| Vermont | 50/100 | 10 |

| Virginia | 25/50 | 20 |

| West Virginia | 25/50 | 25 |

| Wisconsin | 25/50 |

Learn More About Your Auto Insurance

How to read auto insurance coverage levels

UM/UIM limits are often written like liability limits using shorthand split limits:

Bodily injury per person / bodily injury per accident / property damage per accident

Because UM does not always include property damage, you’ll commonly see only bodily injury numbers (for example, “25/50” equals $25,000 per person and $50,000 per accident for UMBI). Where UMPD is offered, it may appear as a separate per‑accident limit with a deductible (often around $250) and may not apply to all hit‑and‑runs. If UMPD is unavailable or limited in your state, collision coverage typically pays for your vehicle’s damage after a deductible (Progressive; Texas Department of Insurance).