Did you know that two identical car insurance policies, for the same driver, can vary by hundreds of dollars depending on the insurance company that sells them? Recent comparisons show large, actionable spreads between companies in 2025: independent datasets find the cheapest large carrier can be hundreds to over $1,000 per year less than the most expensive for comparable “good driver, full coverage” profiles (Bankrate; ValuePenguin). State regulator tools illustrate even bigger gaps for specific ZIP codes and standardized drivers—some scenarios show the highest quote several times the lowest for the same limits (Washington OIC sample rates; Maryland Insurance Administration survey).

This is because every insurer has a unique underwriting formula. (“Underwriting,” in short, is the equation a company plugs your personal information into to figure out how risky you are as a customer.) Insurers weigh factors like age, location/ZIP, driving and claims history, vehicle and annual mileage, and—where allowed—credit-based insurance scores and participation in telematics/usage-based programs differently, so the same profile can return very different prices (Insurance Information Institute; NAIC; rising UBI adoption noted in J.D. Power). Each formula is going to evaluate your risk factors a little differently, and spit out a higher or lower quote depending on that analysis.

The good news is, it’s easy enough to work the system when you’re looking for cheap car insurance. Many direct carriers now return a preliminary auto quote “in minutes” (often about 5–10 minutes for a single driver/vehicle), and marketplaces can show multiple options in one session (GEICO; Progressive; The Zebra). Industry studies also emphasize faster, low-friction digital quoting as a key satisfaction driver (J.D. Power Digital Experience).

Most People Don’t Compare Rates as Often as They Should

Shopping around is one of the best (and easiest) ways to save money on your car insurance. Re-shopping at renewal and requesting quotes from at least three to five providers can meaningfully cut your bill—especially because company-to-company spreads commonly exceed $500–$1,000 per year for comparable coverage (Bankrate; ValuePenguin).

Despite the benefits, many drivers still don’t check annually. The 2025 J.D. Power Insurance Shopping Study reports that about one-third of customers shopped in the past 12 months and roughly one in eight to one in seven (about 12%–14%) switched carriers. Marketwide trackers echo elevated activity but imply that approximately 65%–70% did not shop over the last year (LexisNexis Insurance Demand Meter). Consumer surveys further show that about 25%–40% self‑describe as “rarely or never” shopping (The Zebra).

Context update (2024–2025): Industry sources indicate roughly one‑third of drivers shopped and about 12%–14% switched in the last 12 months; about 65%–70% did not shop annually, and ~25%–40% say they rarely/never shop (J.D. Power; LexisNexis; TransUnion; The Zebra).

People who don’t compare car insurance rates often end up sticking with the same provider year after year. Even with record shopping, the share who actually switched stayed in the low‑teens (about 12%–14%)—so most customers remained with their current insurer. Self‑reported surveys also show close to half say they shopped in the past year and many more plan to shop soon, primarily due to premium increases (TransUnion; J.D. Power 2025).

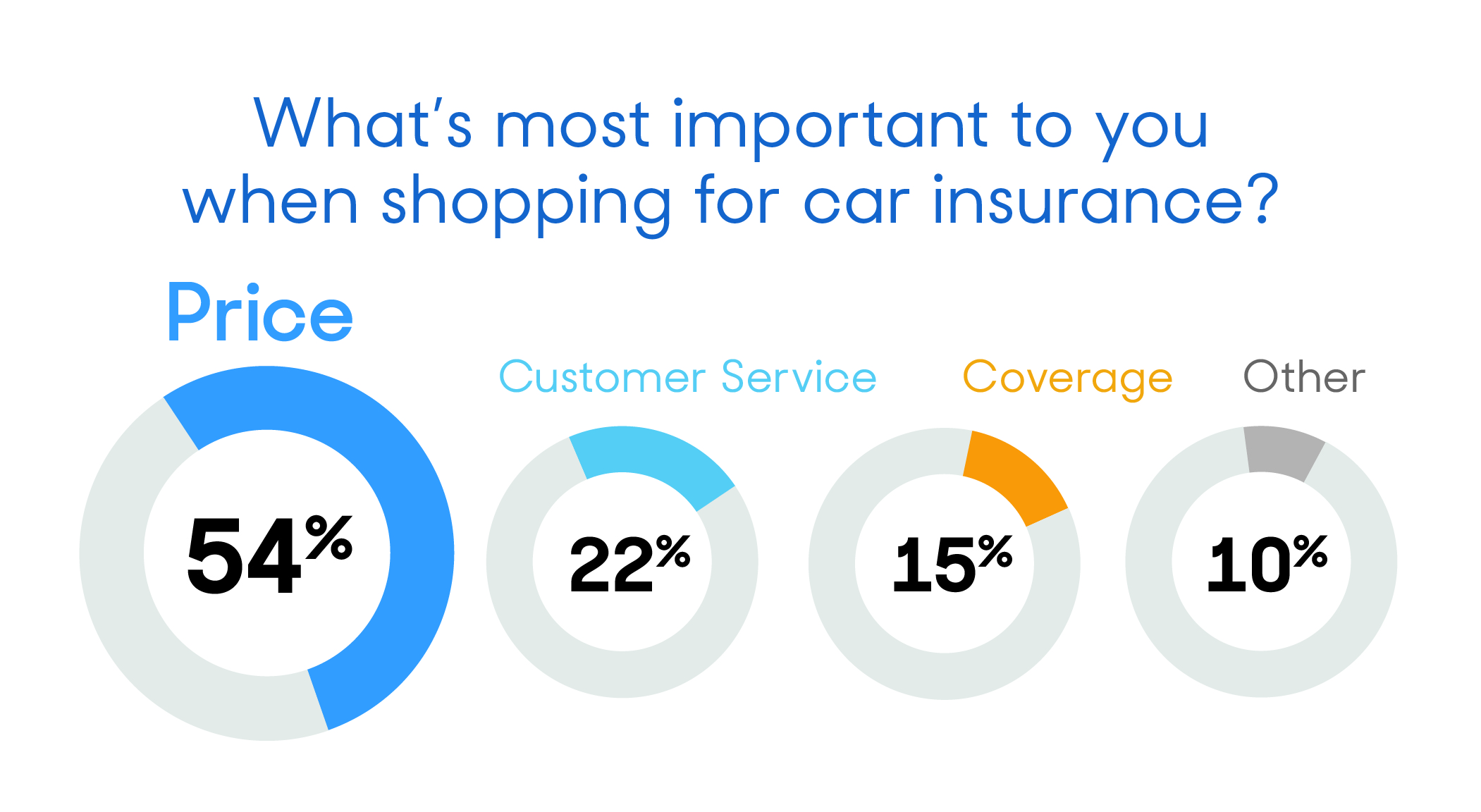

The Funny Thing Is, Most People Care About Rates a Lot

Affordability is the dominant priority today. Motor vehicle insurance inflation has been running in the high teens year over year, keeping price front and center (U.S. Bureau of Labor Statistics). The 2025 J.D. Power Shopping Study and TransUnion’s 2025 trends both find that premium increases are the top reason consumers shop or switch, and that participation in telematics/usage-based insurance is a growing savings lever for price‑sensitive drivers.

What matters most in 2024–2025: Affordability leads, but claims/service quality, coverage fit, discounts/UBI, and digital convenience heavily influence who wins the bind and the renewal (Deloitte; Bain; J.D. Power 2025).

Still, many drivers remain with their current company because overall value feels right—bundled pricing and discounts, acceptable premiums, and confidence in service. Research consistently shows claims experience (speed, fairness, communication) is the strongest driver of loyalty and advocacy, which helps explain why some consumers stay even when shopping is up (Bain; Deloitte).

Among customers who stay, trusted service and easy digital‑plus‑agent support often rank alongside price as retention factors, while others delay shopping because they’re uncertain where to start—despite widespread premium pressure (J.D. Power 2025; TransUnion 2025).

Here’s How Often You Should Be Checking Rates

No matter which camp you sit in (okay with your rates, happy with customer service, daunted by the prospect of finding a new insurer), we recommend checking quotes at each renewal. Carrier appetites and rate filings change frequently, so the cheapest company this term may not be next term (LexisNexis Insurance Demand Meter).

If you’re thinking “There’s no way I’m going to check rates every year,” at least note the times when it’s most important to shop around.

Some major life events will have a big impact on your car insurance rates. If you’ve recently passed one of these milestones, be sure to compare rates next time your policy is up: factors like location, driver age, violations/claims, changes in commute or annual mileage, and—where permitted—credit-based insurance score shifts all commonly trigger re‑rating. Telematics enrollment can also move your price up or down based on actual driving (III; NAIC; J.D. Power on UBI).

- Moved to a new city or ZIP (location strongly affects pricing)

- Added a teen driver to your policy (often the largest premium impact)

- Added another car to your policy or changed vehicles

- Passed the three-year mark after an accident

- Had an accident under your current insurance (or received a ticket)

- Passed a big birthday (20, 25, 30, etc.) affecting age-based pricing

- Got married or divorced (marital status may be a factor where allowed)

How Long Does it Take to Check Car Insurance Quotes?

Comparing insurance prices every year might sound like a hassle. But believe it or not, it only takes a few minutes to get an online quote from most providers—often around 5–10 minutes for a single driver/vehicle with basic coverage needs (GEICO; Progressive; J.D. Power Digital Experience).

To compare multiple options, you can use a marketplace to view several prices in one session (The Zebra) or enter your details on 3–5 carrier sites. Expect roughly 20–60 minutes total depending on your drivers/vehicles and whether a bindable price requires brief follow‑up—experiences vary by carrier, data prefill, and whether quotes are estimates or final bindable offers (J.D. Power Digital Experience).

Don’t worry, asking around for car insurance quotes won’t hurt your credit score when a soft inquiry is used—standard for insurance quote checks (CFPB; FICO; TransUnion). That holds true for an online quote.

It’s also worth mentioning that getting an online quote is 100% free. Major insurers advertise free quotes, and typical insurance quote checks use soft inquiries that don’t affect your credit score (GEICO; FICO).

Of Course, Price Isn’t All That Matters — Use These Resources to Vet Your Provider Before You Buy

Finding a car insurance policy that fits into your budget will likely be your highest priority, and for good reason—premiums have been rising, and affordability is the top driver of shopping and switching (BLS CPI; J.D. Power 2025).

But affordability isn’t all that matters when it comes to car insurance. Balance low premiums with strong claims handling, service quality, and a trusted brand with solid financial backing—factors that drive advocacy and retention even in a price‑sensitive market (Bain; Deloitte).

Check out some of the resources we’ve put together to help you find a car insurance company that are both reputable and budget-friendly: